Earth Observation and AI for Insurance: Improving Risk Assessment, Underwriting, and Claims Analysis

Climate change, increasing weather volatility, environmental degradation, and expanding infrastructure are introducing new layers of uncertainty for the insurance sector. Events such as wildfires, floods, landslides, and storm damage are becoming more frequent and harder to predict using static historical models alone.

How Earth Observation and AI Are Transforming Risk Assessment in the Insurance Sector

The insurance industry has always relied on understanding risk. Traditionally, this has been achieved through historical loss records, catastrophe models, field inspections, and statistical analysis. However, the nature of risk is evolving rapidly.

Earth Observation (EO) data and Artificial Intelligence (AI) are emerging as powerful tools that allow insurers and reinsurers to better understand environmental risk and improve decision-making across the insurance lifecycle.

The Limitations of Traditional Risk Assessment

Most underwriting and risk modelling processes still rely heavily on historical datasets and generalised risk maps. While these tools remain valuable, they often struggle to capture rapid environmental changes that can significantly influence risk exposure.

For example:

- Forest conditions and vegetation density can change quickly, increasing wildfire risk.

- Urban expansion can alter flood exposure in previously low-risk areas.

- Soil moisture, rainfall patterns, and land deformation can affect landslide probability.

- Coastal subsidence and land movement may increase infrastructure vulnerability.

Traditional models typically update slowly, while environmental risk can evolve in near real time. This is where Earth Observation offers a major advantage.

What Earth Observation Data Brings to Insurance

Earth Observation refers to satellite-based monitoring of the Earth’s surface using optical, radar, and multispectral sensors. Programs such as the Copernicus Sentinel satellites, along with commercial Earth Observation systems, generate large volumes of environmental data covering the entire planet.

These datasets allow insurers to observe and measure environmental conditions continuously across large geographic areas.

Examples of insights derived from satellite data include:

- Vegetation health and dryness indicators relevant to wildfire risk

- Flood extent and water accumulation patterns

- Ground deformation and land subsidence affecting infrastructure

- Soil moisture and rainfall trends influencing landslides

- Land use changes that alter exposure profiles

When combined with AI and geospatial analytics, these datasets can be transformed into actionable risk intelligence.

Supporting Key Insurance Workflows

Earth Observation and AI can support multiple stages of the insurance value chain.

1. Risk Assessment and Underwriting

Satellite-derived environmental indicators can help insurers assess the exposure of insured assets before issuing or renewing policies.

For example:

- Identifying properties located near high wildfire risk vegetation zones

- Detecting flood-prone areas based on topography and historical water accumulation

- Evaluating landslide susceptibility based on terrain slope, soil moisture, and land cover

- Monitoring land subsidence affecting buildings, pipelines, or transport infrastructure

- Veryfying long term historical data to detect any seasonality and long-term changes.

This enables more informed underwriting decisions based on current environmental conditions, not only historical risk maps.

2. Portfolio Level Risk Monitoring

Large insurers and reinsurers often manage portfolios distributed across multiple countries or continents. Monitoring risk exposure across such large areas can be difficult using traditional inspection methods.

Satellite data allows organizations to monitor environmental risk at scale, providing insights across entire regions or portfolios.

This can support:

- Early identification of emerging environmental hazards

- Continuous monitoring of insured assets

- Improved catastrophe exposure modelling

- Better climate risk analysis for long-term strategy

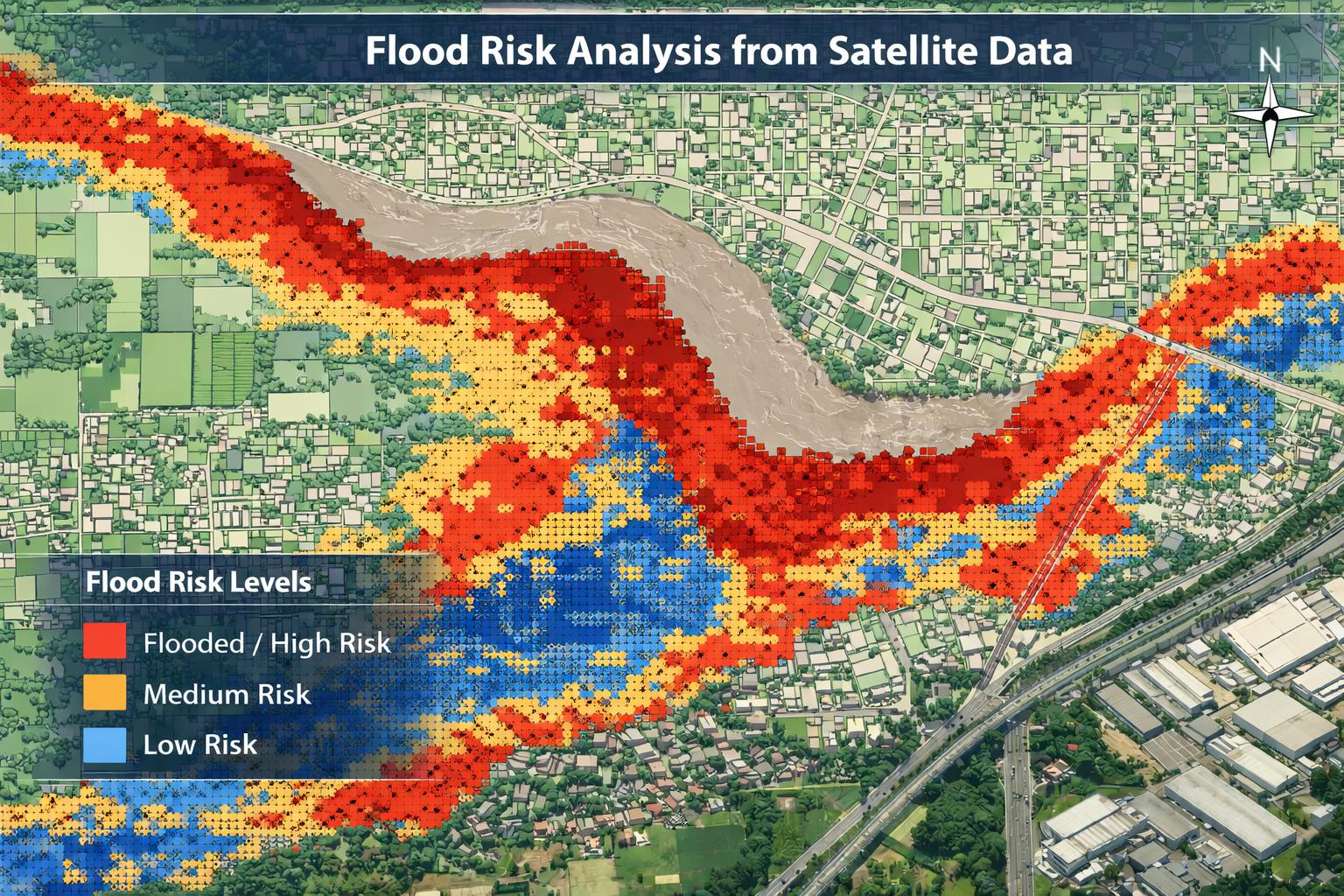

3. Claims Validation and Damage Assessment

Following extreme events such as floods, storms, or landslides, insurers must rapidly assess damages across potentially large areas.

Satellite imagery can help identify and verify:

- Flood extent and affected properties

- Forest damage caused by windstorms

- Landslide-affected infrastructure corridors

- Changes in land cover indicating damage

This can support faster claims assessment and improved transparency, especially in areas where ground inspections may be difficult or delayed.

4. Enabling Parametric Insurance Products

Earth Observation also plays a growing role in parametric insurance, where payouts are triggered automatically when predefined environmental thresholds are exceeded.

Examples include:

- Rainfall levels exceeding flood thresholds

- Wind speeds above storm damage limits

- Vegetation stress indicators linked to drought conditions

- Soil moisture anomalies affecting agriculture

Satellite data provides an objective and verifiable source of environmental measurements, making it well-suited for these types of insurance products.

The Importance of Tailored Risk Intelligence

While global risk platforms and generic models provide useful baseline insights, insurance portfolios and operational workflows vary significantly between organizations.

Different insurers may require:

- Risk indicators tailored to specific asset classes

- Regional or country-specific environmental analysis

- Custom thresholds aligned with underwriting policies

- Flexible data formats that integrate with internal systems

This is why customized Earth Observation analytics can often provide more relevant insights than generic global models.

Our Approach

At SPACE-SHIP, we develop tailored solutions that combine Earth Observation data, geospatial analytics, and AI to support the insurance sector.

Our capabilities include:

- Environmental risk analysis using satellite data

- AI-based hazard monitoring for floods, wildfires, landslides, and storms

- Land subsidence and infrastructure monitoring

- Portfolio-level environmental intelligence for insurers and reinsurers, including long term change studies

- Satellite-based analytics supporting parametric insurance models

Rather than offering one-size-fits-all risk models, we work closely with organizations to design solutions aligned with their specific business needs, data workflows, and risk assessment strategies.

Exploring the Potential

If you are interested in exploring how satellite data could support your underwriting, risk monitoring, or claims workflows, we would be happy to discuss your use case.

We offer a free, non-binding consultation to explore how Earth Observation and AI can support your risk analysis needs.

Conclusion

Earth Observation and AI are not replacing traditional insurance analytics. Instead, they provide a new layer of environmental and business intelligence that allows insurers to better understand how risk is evolving in the physical world and make informed decisions.

As climate-related hazards become more complex, the ability to monitor environmental conditions continuously and analyze them at scale will become increasingly important.